Disclaimer: This article was originally published by Machinery Intelligence Station. Sources: https://mp.weixin.qq.com/s/vFzpzIhSqD2E3rivzxzbUQ. The material for this article comes from foreign media reports.

The Russian road compaction machinery market has an average capacity of 3,000 units. Fluctuating with the economy, the actual market capacity wavers between 1,000 to 3,500 units, with imported road rollers consistently occupying the majority of the market. Previously dominated by European, American, and a few Japanese firms, today it’s Chinese enterprises—XCMG, Liugong, Lingong, Shantui, and SANY among others—that have swiftly taken over three-quarters of the market share. The remaining quarter is split between Russian brands and Western brands.

Experts estimate that Russia’s engineering construction equipment market for road building machinery fell by 7%-10% in 2024 compared to 2023 and is expected to continue a downward trend into 2025. This decline is closely linked to the decrease in funding within civilian economic sectors due to high-interest rates, investment outflow from civil sectors, commodity price volatility, a tight labor market, and traditional fiscal policies, which have hardly stimulated R&D and production investment. The road roller market heavily depends on large-scale infrastructure projects, which, since the end of 2024, have dwindled, reducing the demand for new machinery.

In 2023, the market for road rollers was at 2,595 units, compared to 3,543 the previous year. Russian manufacturers accounted for just over one-tenth of the market, with almost all the rest being products made in China.

Russian machinery manufacturing is primarily represented by factories in Ribinsk, Yaroslavl region: “РАСКАТ” and “Road Machinery Factory.” According to data from 2023, Russian production accounted for a 12% market share. Chinese suppliers dominated with a 75% share, with five providers accounting for 66% of that figure—namely XCMG, Liugong, Lingong, Shantui, and SANY. Despite sanctions, Western brands still held onto 10% of the market. Although final data for 2024 is not yet available, the order of participants is likely to remain unchanged as the numbers decrease.

XCMG Group leads the Russian road roller market, holding a 22% share. Their products are supplied from a large and modern production base located in Xuzhou, encompassing a full range of roller parts and road compaction machinery.

Rusbusinessavto, representing Lingong’s road rollers in Russia along with their own BULL brand, is second in market share at 17%. The Lingong offering includes mechanically and hydraulically driven units suited for various specifications and configurations.

Rusbusinessavto is also expanding their BULL brand of engineering construction equipment, including all-drive soil compactors (14-36 tons) equipped with Weichai engines, 13-ton double drum rollers, and pneumatic rollers weighing 16 and 20 tons featuring a 105 kW Weichai engine.

Liugong is third, with a 16% stake in the market, providing a full range of road rollers including soil, pneumatic, and double drum rollers. Their articulated asphalt rollers come in various models, weighing from 9.5 to 14 tons, featuring two smooth drive drums. Both models employ dual amplitude hydraulic driven vibratory mechanisms, driven by Cummins engines, much like their hydrostatic transmission.

Furthermore, the company offers up to 4-ton sidewalk compactors and manually controlled mini rollers weighing up to 860 kilograms, suitable for compacting small areas of soil and asphalt as well as patching potholes.

Western brands rank fourth at a 10% market share, with Ribinsk’s “Road Machinery Factory” sitting in the fifth spot. If production at this factory exceeds 200 units in 2025, and horizontal imports reduce, it may surpass the suppliers of “unfriendly countries.”

Currently, the factory produces 14-ton and 16-ton soil compactors, double drum vibratory rollers from 7.7 to 13 tons, pneumatic rollers up to 15 tons, and sidewalk rollers ranging from 1.5 to 3 tons.

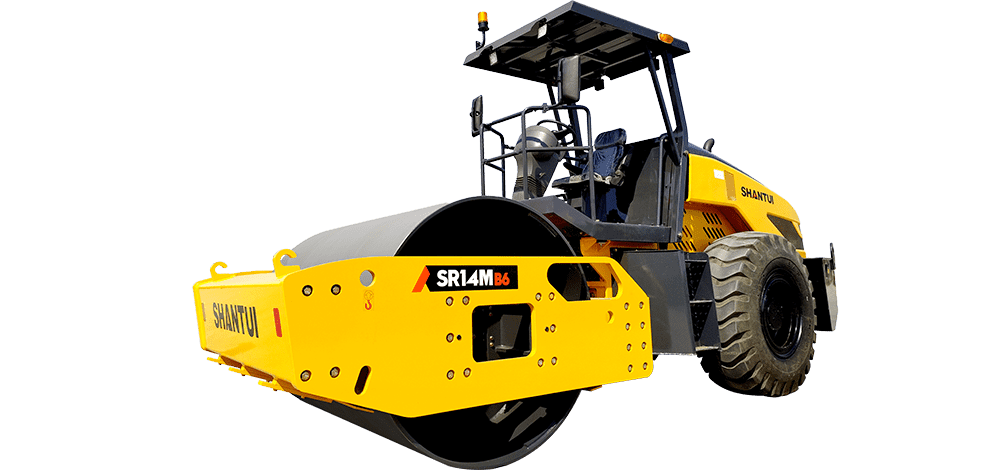

Shantui’s roller parts are in sixth place with a 7% market share, offering soil compactors from 10 to 26 tons, double drum rollers from 7 to 14 tons, and pneumatic rollers between 16 and 30 tons.

SANY Heavy Industry ranks seventh with a 4% market share, providing rollers since the 2000s, with a recent push including soil vibratory compactors from 10 to 26 tons and double drum rollers from 3 to 14 tons.

Russia’s oldest roller manufacturer “РАСКАТ” ranks eighth with a 2% market share, producing soil compactors from 13 to 21 tons and double drum rollers from 7.5 to 14 tons.

Thus, Chinese enterprises fully meet the needs of Russian road and dam builders. Russian factories have almost no chance of direct competition in the market, surviving only through protectionist measures. Furthermore, excessive protectionism could lead to a lack of pressure on large construction projects since two factories are unable to meet the entire demand. The issue lies not only in production capacity but also in the availability of components.

Keywords: